Are you a UAE business owner, finance manager, or startup founder? This guide explains UAE transfer pricing rules and helps you avoid compliance pitfalls—no jargon, just actionable answers for your business.

Key Points:

- Related parties = businesses or people with close ties (ownership, family, or control)

- UAE rules differ from international standards—don’t rely on global policies

- Accurate identification and disclosure avoids penalties

- BCL offers practical, step-by-step support for every business size

Overview of UAE Transfer Pricing Regulations

The UAE introduced comprehensive transfer pricing regulations through Federal Decree-Law No. 47 of 2022, aligning with OECD guidelines. These rules ensure that transactions between related parties are conducted at arm’s length prices, preventing profit shifting and maintaining fair tax collection. The regulations apply to all UAE corporate tax residents and cover various transaction types including goods, services, intellectual property, and financing arrangements.

Understanding UAE Transfer Pricing Related Parties

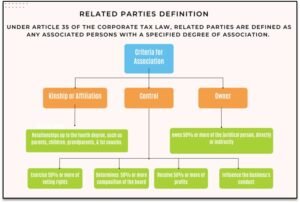

WHO ARE RELATED PARTIES?

If you own or manage a business in the UAE, a ‘related party’ means anyone—company or individual—who has a significant connection to your business, like through ownership, control, or family ties. This relationship may arise through ownership, control, or kinship (for individuals).

To ensure compliance, you must identify your related parties as defined in Article 35 of the UAE CT Law, with additional guidance provided in the UAE Transfer Pricing (TP) Guidelines. It is crucial to recognize that the definition of related parties under UAE TP regulations differs from the criteria set out in International Accounting Standard (IAS) 24: Related Party Disclosures.

Transfer Pricing Rules and Arm’s Length Principle

The arm’s length principle (the standard for fair pricing between related parties) is the cornerstone of UAE transfer pricing regulations. This principle requires that transactions between related parties be priced as if they were conducted between unrelated parties under similar circumstances. The UAE follows OECD guidelines in applying this principle, ensuring that related party transactions reflect market conditions and prevent artificial profit shifting.

Key Rules for Related Party Transactions under UAE Transfer Pricing

Related party transactions UAE corporate tax rules require businesses to ensure that all transactions between connected entities follow the arm’s length principle (the standard for fair pricing between related parties). Companies must maintain proper documentation and comply with transfer pricing regulations issued by the UAE authorities. Non-compliance can result in penalties and increased scrutiny during tax assessments.

These differences impact how related parties are identified and treated under each framework. Consequently, businesses operating in the UAE should conduct a thorough assessment based on UAE TP rules rather than relying solely on financial statement disclosures or global TP policies.

For a comprehensive understanding of the UAE’s transfer pricing regulations and disclosure requirements, refer to our detailed guide

Transfer Pricing Methods Accepted in the UAE

The UAE recognizes six standard OECD transfer pricing methods for determining arm’s length prices:

- Comparable Uncontrolled Price (CUP) Method: Compares prices charged in controlled transactions with those in comparable uncontrolled transactions

- Resale Price Method (RPM): Based on the price at which a product is resold to an independent enterprise

- Cost Plus Method (CPM): Adds an appropriate markup to the costs incurred by the supplier

- Transactional Net Margin Method (TNMM): Examines net profit margins relative to an appropriate base

- Transactional Profit Split Method (PSM): Allocates combined profits based on each party’s contribution

- Other Methods: Alternative approaches when traditional methods are not suitable

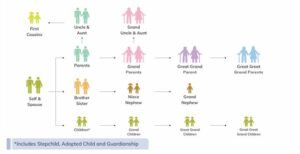

- Kinship and Affiliation (natural persons[1])

- Two or more individuals related to the fourth degree of kinship or affiliation, including by birth, marriage, adoption, or guardianship.

- Kinship*—each step from a common ancestor that describes the level of relationship between two blood-related persons, such as first cousins, one sibling to another, parent to child.

- Affiliation: the state of being closely associated with or connected to an organization

* Generally, a first degree, second degree, third degree, or fourth degree kinship or relative of the individual means

|

Degree |

Relationship |

|

First-degree |

Parents, siblings, and children |

|

Second-degree |

Grandparents, grandchildren, uncles, aunts, nephews, nieces, and half siblings |

|

Third-degree |

Great-grandparents, great-grandchildren, great-uncles/aunts, and first cousins |

|

Fourth-degree |

Great great-grandparents, great-great-grandchildren, and first cousins once removed |

- Ownership / Control

- An individual and a legal entity where the individual, alone or with a related party, directly or indirectly owns or controls at least 50% of the entity.

- Two or more legal entities where one entity, alone or with a related party, directly or indirectly owns or controls at least 50% of the other.

- Two or more legal entities if a taxpayer alone, or with a related party, directly or indirectly owns a 50% share of each or controls them.

- Control

- Control means having the ability to influence another person or entity. This can be through:

- Voting Rights: holding 50% or more of the voting rights.

- Board of Directors: being able to determine 50% or more of the board’s composition.

- Profit Sharing: receiving 50% or more of the profits.

- Significant Influence: Exercising significant influence over the business and its affairs.

- Other Scenarios

- Includes relationships like a person and their Permanent Establishment, partners in the same unincorporated partnership, and connections through trusts or foundations.

Learn about the Country-by-Country Reporting requirements and how they relate to related party transactions.

Transfer Pricing Documentation Requirements

UAE businesses must maintain comprehensive transfer pricing documentation to demonstrate compliance with the arm’s length principle:

|

Document Type |

Threshold |

Deadline |

|

Master File |

AED 3.15 billion consolidated revenue |

12 months after tax period end |

|

Local File |

AED 200 million revenue |

12 months after tax period end |

|

Disclosure Form |

AED 200 million revenue |

With CT return filing |

|

Country-by-Country Report |

AED 3.15 billion consolidated revenue |

12 months after tax period end |

IDENTIFICATION OF RELATED PARTIES UNDER UAE TRANSFER PRICING REGULATIONS

Practical Identification Checklist:

- Review ownership structures and shareholding patterns

- Map family relationships up to fourth degree of kinship

- Analyze control mechanisms (voting rights, board composition)

- Document trust and foundation relationships

- Consider permanent establishment connections

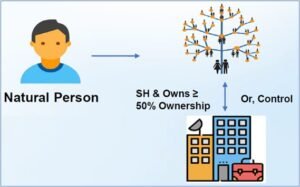

- Natural person [Article 35(1)(a)]

- Related within the fourth degree of kinship or affiliation, including relationships established through adoption or guardianship

- Natural person and Juridical Person [Article 35(1)(b)]

- A Natural Person (NP) or at least one Related Party (RP) of the NP holds shares in a Juridical Person[2] (JP), and the NP, either individually or together with its RP, directly or indirectly owns 50% or more of the ownership interest in the JP.

- The NP, either alone or in combination with its RP, directly or indirectly controls the JP.

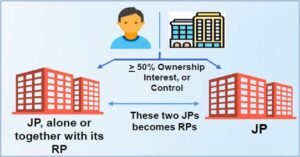

- Two or more juridical persons (legal entity) [Article 35(1)(c)]

-

- A Juridical Person (JP), either independently or in conjunction with its Related Party (RP), directly or indirectly holds 50% or more ownership interest in another Juridical Person (JP).

-

- A Juridical Person (JP), either independently or in conjunction with its Related Party (RP), directly or indirectly controls another Juridical Person (JP).

-

- Any Person, either independently or in conjunction with its Related Party (RP), directly or indirectly owns 50% or more ownership interest in, or controls, two or more Juridical Persons (JPs).

- A Person and its Permanent Establishment or Foreign Permanent Establishment [Article 35(1)(d)]

- Two or more Persons that are partners in the same Unincorporated Partnership. [Article 35(1)(e)]

- A Person who is the trustee, founder, settlor, or beneficiary of a trust or foundation and its Related Parties. [Article 35(1)(f)]

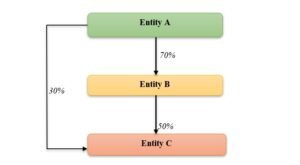

Example of Related Parties under UAE CT Law

*Ownership of a legal entity encompasses voting rights, a share in profits, and authority over the composition of the board.

-

- Entity A and Entity B are considered related entities due to Entity A holding a majority ownership share in Entity B.

- Similarly, Entity A and Entity C are related through a combination of direct and indirect ownership. Entity A holds an indirect ownership of 35% in Entity C via its 70% stake in Entity B (70% x 50%) and a direct ownership of 30%, resulting in a total ownership interest of 65%, which exceeds the 50% threshold.

-

Furthermore, Entity B and Entity C are related as they are both affiliated with Entity A.

To understand how related party transactions fit within the broader corporate tax framework, consult our UAE Corporate Tax Guide.

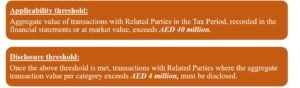

Transfer Pricing Disclosure Form and Reporting Requirements

The RPT Schedule (Schedule 16) is a part of the TP Disclosure Form, which forms the first section of the UAE Corporate Tax (CT) Return. It requires the disclosure of high-value transactions with related parties, as defined in Article 35 of the UAE CT Law, when prescribed thresholds are met. This schedule includes details such as party name, country, transaction type, gross value, TP method used, arm’s length value, and any tax adjustments. All transactions with related parties must be reported, covering categories like goods, services, intellectual property, interest, assets, liabilities, and others.

Stay informed about the reporting deadlines to ensure timely compliance with UAE transfer pricing regulations.

Disclosure requirements

- 1.5 | Gross Income/Expenses

This field requires the Gross Income Earned (Revenue before any Deductions), or Expenses Incurred in relation to the transaction with such Related Party. The UAE TP Disclosure Form requires reporting the full gross value of related party transactions before any adjustments. This means reporting the total transaction amounts without netting off or reducing by discounts or rebates.

- 1.6 | Transfer Pricing Method

The UAE TP Disclosure Form allows selection of six standard OECD transfer pricing methods: The Comparable uncontrolled price method (CUP), the resale price method (RPM), the cost-plus method (CPM), the transactional net margin method (TNMM), the transactional profit split method (PSM), and the other method.

Explore the various transfer pricing methods applicable in the UAE to make sure accurate and compliant reporting.

- 1.7 | Arm’s Length Value

This field requires the Arm’s Length Value of the Related Party Transaction (the value which would have been if such Party were not a Related Party).

- 1.8 | Tax Adjustment

This field is calculated automatically based on the difference between Gross Income/Expenses and Arm’s Length Value. This can be an upwards or downwards adjustment as mentioned below. The “Tax adjustment” field in the UAE TP disclosure form represents the difference between the actual transaction value and the arm’s length value. It’s the amount by which the taxable income would need to be adjusted to reflect arm’s length pricing. This field helps tax authorities understand the potential impact of transfer pricing on the entity’s tax liability.

For detailed information on the disclosure requirements for related party transactions, refer to our comprehensive guide on Transfer Pricing Disclosure Requirements.

Penalties for Non-Compliance

UAE transfer pricing non-compliance can result in significant penalties and increased scrutiny from the Federal Tax Authority (FTA):

- Late Filing Penalties: AED 10,000 for late submission of transfer pricing documentation

- Inaccurate Information: Additional penalties for providing incorrect or incomplete information

- Primary Adjustments: Tax adjustments to reflect arm’s length pricing

- Secondary Adjustments: Deemed distributions or benefits for non-arm’s length transactions

- Increased Audit Risk: Enhanced scrutiny and detailed reviews by tax authorities

KEY TAKEAWAYS

- Properly identify related parties per UAE law using Article 35 criteria

- Maintain arm’s length pricing and detailed documentation for all related party transactions

- Ensure timely filing of disclosure forms and supporting documentation

- BCL can guide you through compliance painlessly with expert support

Compliance Checklist:

- Map all related party relationships using UAE criteria

- Document transfer pricing methods and benchmarking

- Prepare Master File and Local File (if thresholds met)

- Complete disclosure form with CT return

- Review and update annually

The definition and identification of related parties under the UAE CT Law are crucial for businesses to ensure compliance with the new regulations. Understanding the distinctions between related party criteria under UAE Transfer Pricing rules and international frameworks is essential to properly assess business relationships. Additionally, the requirement to maintain Arm’s Length Price (ALP) (the standard for fair pricing between related parties) and submit a Transfer Pricing Disclosure Form (DF) ensures transparency, particularly when related party transactions exceed specified thresholds. By adhering to these regulations, businesses can navigate the evolving tax landscape, minimize risks, and contribute to the UAE’s broader fiscal objectives.

Avoid common pitfalls in tax compliance by reading our article on Common Tax Mistakes Businesses Make and How to Avoid Them.

Frequently Asked Questions about UAE Transfer Pricing

Does the UAE have transfer pricing regulations?

Yes, the UAE introduced comprehensive transfer pricing regulations through Federal Decree-Law No. 47 of 2022, effective from June 1, 2023. These regulations align with OECD guidelines and apply to all UAE corporate tax residents.

What is the arm’s length principle in UAE transfer pricing?

The arm’s length principle requires that transactions between related parties be priced as if they were conducted between unrelated parties under similar circumstances. This ensures fair market pricing and prevents artificial profit shifting.

Who needs to comply with transfer pricing rules in the UAE?

All UAE corporate tax residents with related party transactions must comply. Specific documentation requirements apply to businesses with revenue exceeding AED 200 million, while Master File and Country-by-Country reporting apply to larger multinational groups.

What are the penalties for non-compliance with UAE transfer pricing?

Penalties include AED 10,000 for late filing, additional penalties for inaccurate information, primary and secondary tax adjustments, and increased audit scrutiny from the Federal Tax Authority.

HOW BCL GLOBIZ CAN HELP?

- Related Party Analysis: We help you identify related parties and connected persons under UAE-specific TP rules, ensuring compliance with Federal Decree-Law No. 47 of 2022 and TP Guidelines.

- Documentation Support: We prepare robust TP documentation aligned with OECD guidelines and UAE regulations to meet statutory requirements. Understand the components of the Master File and its role in transfer pricing documentation.

- Compliance Assurance: We ensure your business adheres to UAE TP regulations, avoiding penalties and fostering smooth interactions with the Federal Tax Authority (FTA).

- Customized Solutions: We offer practical strategies to manage tax and TP risks, leveraging our expertise in UAE and international tax regimes.

- Ongoing Support: We provide continuous updates and advisory on regulatory changes and their implications for your operations.

Why Choose BCL Globiz?

- UAE’s leading firm with specialized transfer pricing expertise

- Dedicated WhatsApp support for every client

- 100% Refund Guarantee—risk-free engagement

- Trusted by 500+ UAE businesses across all sectors

- Comprehensive, all-inclusive packages with transparent pricing

[1]Natural Person: Individual human being (distinct from a juridical person).

Person: Any Natural Person or Juridical Person.

[2]The guide confirms that juridical person (also referred to as Free Zone (FZ) Person), i.e., incorporated, established, or otherwise registered in a FZ, including a branch of a Non-Resident Person or a UAE juridical person that is registered in a FZ.

Discover how proactive transfer pricing strategies can benefit your business beyond compliance.